Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Central banks are starting to tip-toe away from the emergency stimulus they deployed to fight the pandemic-driven global recession.

Federal Reserve Chair Jerome Powell and colleagues have begun debating when and how to slow their asset-purchase program, while the People’s Bank of China is already curbing credit growth. Brazil, Mexico, Turkey, the Czech Republic and Russia have hiked interest rates and others are starting to publicly detail how they may pull back support.

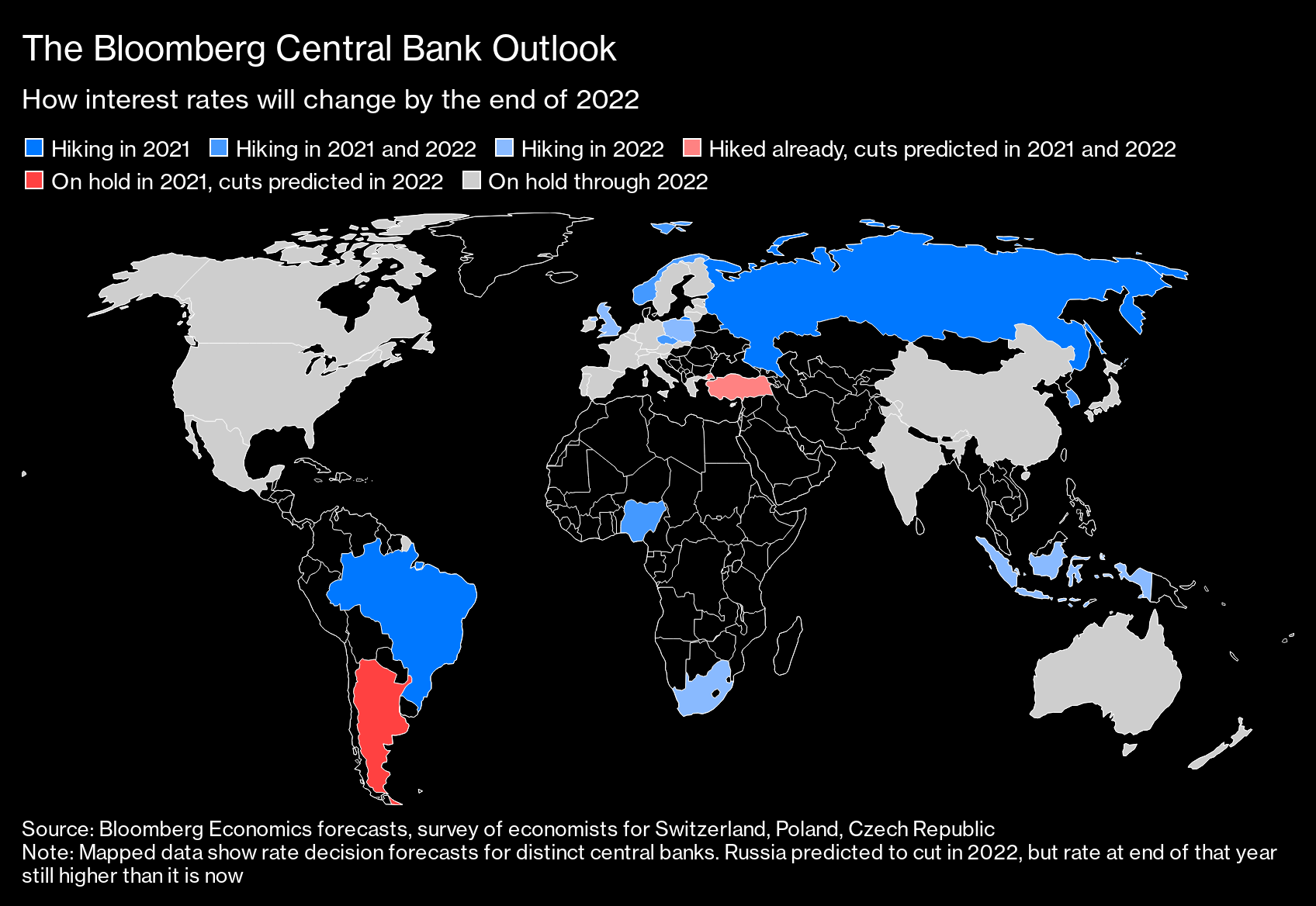

The Bloomberg Central Bank Outlook

How interest rates will change by the end of 2022

Source: Bloomberg Economics forecasts, survey of economists for Switzerland, Poland, Czech Republic

Note: Mapped data show rate decision forecasts for distinct central banks. Russia predicted to cut in 2022, but rate at end of that year still higher than it is now

The global pivot will still be gradual. The European Central Bank and Bank of Japan are likely to keep doling out aid to their economies, while even those turning hawkish still bet the recent surge in inflation will soon pass and are pledging to avoid roiling financial markets. The path of the

delta variant could also still upend sentiment and demand.

Balance sheets will keep expanding, albeit at a slower pace, and borrowing costs will stay close to historic lows.

What Bloomberg Economics Says:

“The near unanimous view from central bankers is that the current bout of high inflation is transitory. In the second half, with Europe, Japan, and India expected to join the U.S. in the rapid phase of the recovery, the definition of transitory may well be stretched, and could be broken.”

--Tom Orlik, chief economist

Here is Bloomberg’s quarterly guide to 23 of the world’s top central banks, covering 90% of the world economy:

GROUP OF SEVEN

U.S. Federal Reserve

- Current federal funds rate (upper bound): 0.25%

- Bloomberg Economics forecast for end of 2021: 0.25%

- Bloomberg Economics forecast for end of 2022: 0.25%

Jerome Powell

Photographer: Andrew Harrer/Bloomberg

Powell has started the discussion about scaling back the Fed’s massive monthly bond purchases and could use its Aug. 26-28 Jackson Hole policy retreat to signal a decision is at hand.

While policy makers don’t expect to raise rates before 2023, seven of 18 last month projected liftoff from current near-zero levels next year amid anxiety over surging inflation.

Recent readings on the U.S. economy have been volatile with supply bottlenecks affecting prices, while job creation has been disappointing. Officials say the data reflects glitches as the economy reopens and expect to have a clearer reading in September.

Inflation is the key variable. Powell and other senior officials argue the spike is likely to prove temporary. But they promise to watch developments and could reassess if longer-term inflation expectations drift higher.

That could bring forward the timing of taper and persuade more officials to pencil in rate hikes in 2022.

What Bloomberg Economics Says:

““The fastest rate of core PCE inflation since 1992 is testing the transitory inflation thesis. With reopening-sensitive categories dominating the rise, a substantial shortfall from maximum employment provides a powerful argument against retracting accommodation too soon. As a result we think QE taper will commence in early 2022, with a first rate hike not until late 2023.”

--Andrew Husby

European Central Bank

- Current deposit rate: -0.5%

- Bloomberg Economics forecast for end of 2021: -0.5%

- Bloomberg Economics forecast for end of 2022: -0.5%

Christine Lagarde

Photographer: Alex Kraus/Bloomberg

The ECB has pledged to keep financing conditions for governments, companies and households “favorable” until the coronavirus crisis phase is over. It’s currently buying bonds under its 1.85 trillion-euro ($2.2 trillion) Pandemic Emergency Purchase Program at an elevated pace, bolstered by negative rates and ultra-cheap long-term loans to banks.

PEPP is due to run until at least the end of March 2022. Yet with inflation forecast to fall short of the just-below 2% target for at least the next two years -- and with a strategy review set to wrap up soon -- the scene is set for a debate over what should replace it.

The euro-area economy turned a corner in the second quarter after vaccinations rose and virus infections fell, allowing governments to lift restrictions. Inflation is forecast to climb well above the ECB’s target toward the end of this year, though President Christine Lagarde, like her counterparts at the Fed, insists the jump is temporary.

What Bloomberg Economics Says:

“The ECB has pledged to buy bonds through its Pandemic Emergency Purchase Programme at a ‘significantly higher pace’ through 3Q. We expect a reversion to the pace of 1Q after September and purchases to end in March 2022. Acquisitions through the Asset Purchase Programme will probably continue until December 2023, six months before the deposit rate is increased by 25 basis points to -0.25%.”

--David Powell

Bank of Japan

- Current policy-rate balance: -0.1%

- Bloomberg Economics forecast for end of 2021: -0.1%

- Bloomberg Economics forecast for end of 2022: -0.1%

Haruhiko Kuroda

Photographer: Kiyoshi Ota/Bloomberg

The BOJ will closely monitor the recovery of the economy as the nation hosts the Olympics this summer and its vaccination drive picks up speed.

The central bank has already extended its pandemic support measures by another six months and made clear it doesn’t expect inflation to even reach its 2% target before 2024. That means rates and asset purchases will stay in place for the foreseeable future.

As expectations grow that stimulus will be reined in elsewhere in the world, a holding pattern in Japan could help to further soften the yen. A weaker currency would boost the profits of the nation’s exporters and import a little more price growth.

That leaves the unveiling of the BOJ’s new climate-focused lending facility as the biggest likely event this quarter.

What Bloomberg Economics Says:

“The BOJ looks set to stay on cruise control, probably through 2022. The closer the Fed comes to raising rates, the closer the BOJ could come to raising its overnight rate to 0% and removing the 0% target for the 10-year JGB yield.”

--Yuki Masujima

Bank of England

- Current bank rate: 0.1%

- Bloomberg Economics forecast for end of 2021: 0.1%

- Bloomberg Economics forecast for end of 2022: 0.25%

Andrew Bailey

Photographer: Simon Dawson/Bloomberg

Britain’s inflation rate is surging, but the BOE has pushed back against mounting expectations it may have pare back the pace of stimulus. Policy makers in June warned against “premature tightening” that could threaten the recovery, noting that a surge in prices above their 2% target for the first time in almost three years will probably be temporary.

For now, officials led by Governor Andrew Bailey, are focused on ensuring that the recovery takes hold, absorbing unemployed and furloughed workers hit by some of the toughest coronavirus lockdown rules in Europe.

What Bloomberg Economics Says:

“The scale of the fallout from the ending of the furlough scheme in September will be key for the BOE’s next move. We expect only a modest rise in joblessness, which will begin to unwind as the recovery continues into 2022. With inflation also near 2%, rates are likely to rise by 15 bps at the end of that year.”

--Dan Hanson

Bank of Canada

- Current overnight lending rate: 0.25%

- Bloomberg Economics forecast for end of 2021: 0.25%

- Bloomberg Economics forecast for end of 2022: 0.25%

Tiff Macklem

Photographer: Sean Kilpatrick/Canadian Press/Bloomberg

The Bank of Canada is half way through its bond tapering, with the next step expected as early as when officials gather July 14. The central bank is among the first from advanced economies to shift to a less expansionary policy, having already cut its purchases of Canadian government bonds to C$3 billion weekly from a peak of C$5 billion last year.

Analysts anticipate that will come down to C$2 billion per week in July, before eventually falling to about C$1 billion by early next year. At that point, attention will turn to debating rate hikes.

What Bloomberg Economics Says:

“Quickening inflation will test the BoC’s ability to break with past patterns of preemptive hikes. A near-full labor market recovery relative to the pre-pandemic trend may not occur until the end of 2022, factoring heavily in our baseline for a first move in 1Q 2023 -- later than markets expect.”

--Andrew Husby

BRICS CENTRAL BANKS

People’s Bank of China

- Current 1-year best lending rate: 3.85%

- Bloomberg Economics forecast for end of 2021: 3.85%

- Bloomberg Economics forecast for end of 2022: 3.85%

Photographer: Qilai Shen/Bloomberg

The rapid recovery from the pandemic has seen China’s central bank shift to a more neutral stance, keeping rates unchanged and providing enough liquidity to financial markets to meet demand. With the economy well on track to exceed the government’s target of ‘above 6%’ growth this year, the PBOC has focused on controlling financial risks by curbing credit expansion. Consumer inflation has been fairly tame so far, with the rapid increase in factory prices mainly fueled by surging commodity prices, which the government is trying to clamp down on.

With the recovery still unbalanced because of a sluggish rebound in consumption, and growth risks building in the second half of the year, the PBOC is proceeding cautiously. Since it’s already ahead of many other central banks in normalizing policy, economists don’t expect the PBOC to tighten even if developed economies start looking at exiting their stimulus programs. Instead, the PBOC will likely allow the yuan to weaken and provide enough liquidity to the financial system.

What Bloomberg Economics Says:

“China has shifted its monetary policy stance to a tightening bias and is draining liquidity to temper credit growth. Our baseline view is that the PBOC has found the sweet spot for interest rates and will stay on hold through 2022.”

--Chang Shu

Source: NBS, PBOC, General Administration of Customs, Bloomberg Economics

Reserve Bank of India

- Current RBI repurchase rate: 4%

- Bloomberg Economics forecast for end of 2021: 4%

- Bloomberg Economics forecast for end of 2022: 4%

Shaktikanta Das

Photographer: Dhiraj Singh/Bloomberg

India is set to keep borrowing costs at a record low this quarter as the central bank’s Monetary Policy Committee focuses on reviving economic growth. The panel, headed by Governor Shaktikanta Das, has signaled it will tolerate higher inflation as it isn’t yet demand driven.

Das, who led the rate panel in cutting borrowing costs by 115 basis points last year, has said that the RBI isn’t thinking about normalization of monetary policy yet. It has kept rates at a record low for more than a year and expanded a bond-buying program aimed at anchoring borrowing costs.

What Bloomberg Economics Says:

“The Reserve Bank of India is likely to accommodate higher cost push inflation in the near term, as it aims to secure the recovery. It is likely to deliver policy easing through sovereign bond purchases to cap longer tenor yields. We expect it to maintain the status quo on rates this year, begin raising the reverse repo rate in early 2022 and a start a gradual repo rate hiking cycle in early 2023.”

--Abhishek Gupta

Central Bank of Brazil

- Current Selic target rate: 4.25%

- Bloomberg Economics forecast for end of 2021: 6.5%

- Bloomberg Economics forecast for end of 2022: 6.5%

Roberto Campos Neto

Photographer: Andre Coelho/Bloomberg

Brazil’s central bank is aggressively raising its key interest rate as the economic recovery gains steam and inflation forecasts remain above target this year and next. Policy makers boosted the benchmark Selic by 75 basis points in each of their past three meetings and signaled that a full percentage point increase may be on tap in August.

The bank board scrapped plans to keep part of its monetary stimulus in place, and now says it aims to bring rates to a neutral level. Futures traders are betting the Selic ends this year above 7% as drought elevates electricity costs and adds fresh pressure to annual inflation that’s already near a five-year high.

What Bloomberg Economics Says:

“High headline, underlying and expected inflation led the BCB to signal an impending end to monetary stimulus. The central bank seems keen on doing whatever it takes to bring inflation expectations for 2022 back to the 3.5% target as soon as possible, even if that means accelerating rate hikes. But high unemployment will likely prevent a shift to tight monetary policy. We expect the Selic to end the year at 6.5% -- a level we see as neutral -- and remain there throughout 2022.”

--Adriana Dupita

Bank of Russia

- Current key rate: 5.5%

- Bloomberg Economics forecast for end of 2021: 6.25%

- Bloomberg Economics forecast for end of 2022: 5.75%

Elvira Nabiullina

Photographer: Andrey Rudakov/Bloomberg

The Bank of Russia raised the benchmark rate to 5.5% in June, bringing the total in hikes this year to 125 basis points. With inflation running well above the bank’s 4% target, Governor Elvira Nabiullina says another rate increase is very likely in July given the fastest inflation in more than four years.

Government efforts to hold back prices with administrative limits have had little effect and inflation is forecast to begin slowing only in the fall.

A wave of Covid-19 cases that has taken infection rates in the capital to record levels has led authorities to reimpose some restrictions, adding to risks to the outlook and potentially limiting the space for further rate hikes.

What Bloomberg Economics Says:

“Further tightening by the Bank of Russia is all but guaranteed. Policy makers don’t have the luxury of looking through transitory price pressure. They’re likely to hike by at least another 75 bps to help get inflation expectations under control.”

--Scott Johnson

Source: Federal Statistics Service, BIS, J.P.Morgan/Markit, Economy Ministry, Bank of Russia, BE

South African Reserve Bank

- Current repo average rate: 3.5%

- Bloomberg Economics forecast for end of 2021: 3.5%

- Bloomberg Economics forecast for end of 2022: 4%

Lesetja Kganyago

Photographer: Jason Alden/Bloomberg

The South African Reserve Bank’s signaling that rate hikes are unavoidable has been vindicated by better-than-projected domestic economic growth in the first quarter, rising inflation expectations since the start of the year and global discussions about tightening.

Inflation at a 30-month high in May is unlikely to bring forward the first rate increase from late 2021 or early 2022, because it was in line with forecasts. However, it could lead the central bank to lift its price-growth forecasts slightly at its next monetary policy committee meeting in July.

What Bloomberg Economics Says:

“The big question now is whether the SARB will start hiking rates in 4Q21 or 1Q22. We see inflation undershooting the SARB’s forecast in 2H, keeping rates on hold through 2021. However, a better-than-expected recovery may set the hiking cycle off as early as the fourth quarter – the SARB already sees the risks to inflation as tilted to the upside, with both the market and its quarterly projection model suggesting the first upward movement in the repo will occur in 4Q.”

--Boingotlo Gasealahwe

MINT CENTRAL BANKS

Banco de Mexico

- Current overnight rate: 4.25%

- Bloomberg Economics forecast for end of 2021: 4.5%

- Bloomberg Economics forecast for end of 2022: 4.5%

Alejandro Diaz de Leon

Photographer: Alejandro Cegarra/Bloomberg

Economists are expecting at least one more rate hike from Mexico’s central bank this year, after it surprised by increasing rates in June for the first time since late 2018. The bank acted after inflation ballooned to more than double the 3% target in April and barely eased through the rest of the quarter.

The bank still says price increases are transitory, but now doesn’t see them nearing their target until the third quarter of 2022. Market expectations for additional hikes have jumped. Inflation has been driven by pandemic-caused shocks in supply chains and economic output, the bank has said, while a drought affecting Mexico also fanned agricultural and livestock prices.

What Bloomberg Economics Says:

“We expect Banxico to hike rates by 25 basis points to 4.5% in the third quarter due to mounting short-term pressure on prices. The possibility of more hikes being necessary while demand and activity are below potential will loom large over the selection of the next central bank governor in December.”

--Felipe Hernandez

Bank Indonesia

- Current 7-day reverse repo rate: 3.5%

- Bloomberg Economics forecast for end of 2021: 3.5%

- Bloomberg Economics forecast for end of 2022: 3.75%

Perry Warjiyo

Photographer: Dimas Ardian/Bloomberg

Bank Indonesia finds itself caught between the nation’s surge in coronavirus cases and the Fed signaling a sooner-than-expected taper. Thanks to the country’s benign inflation rate, Governor Perry Warjiyo has room to deliver another rate cut. But this risks spurring further foreign outflows, which have sent the rupiah tumbling. Ample foreign reserves and a narrow current-account deficit should help it defend the currency.

Southeast Asia’s largest economy is expected to rebound from last year’s contraction, but a return to partial lockdowns will cap the upside. Bank Indonesia will likely look to macroprudential tools to support the economy, with Warjiyo exploring lending measures for the hard-hit retail and hospitality sectors. Monetary tightening isn’t seen until next year, and will likely start with reducing liquidity injections prior to raising rates, Warjiyo said.

What Bloomberg Economics Says:

“Bank Indonesia could justify another rate cut with the inflation outlook benign and recovery prospects dented by a virus outbreak and slow shots. But the rupiah remains vulnerable to selling pressure, precluding a cut. That suggests the central bank will instead lean on other tools to support growth, making the next move in rates a hike -- in 4Q 2022 or later.”

--Tamara Henderson

Central Bank of Turkey

- Current 1-week repo rate: 19%

- Bloomberg Economics forecast for end of 2021: 17%

- Bloomberg Economics forecast for end of 2022: 14%

Sahap Kavcioglu

Photographer: Ali Balikci/Anadolu Agency/Getty Images

Turkey’s central bank is once again under pressure from President Recep Tayyip Erdogan to reduce rates even as a weak lira and higher global commodity prices continue to cloud the inflation outlook. Central bank Governor Sahap Kavcioglu kept rates unchanged for a third month in June but the president renewed his calls for lower rates with July or August as a target date for a cut.

Some economists say the central bank can start delivering a reduction in the benchmark as early as the third quarter, while others argue it may have to wait until the final three months. The lira has weakened against the dollar since Kavcioglu took over in March, even though he’s pledged to work toward a positiv rate when adjusted for realized and expected inflation, and to maintain tight policy until the bank’s 5% inflation target is achieved.

What Bloomberg Economics Says:

“Erdogan has already announced the timing of the next rate cut -- July or August, he said. Given his track record of firing three central bank governors in two years, we should take his guidance seriously. We expect easing to begin in 3Q and the lira to pay the price.”

--Ziad Daoud

Central Bank of Nigeria

- Current central bank rate: 11.5%

- Bloomberg Economics forecast for end of 2021: 12%

- Bloomberg Economics forecast for end of 2022: 14%

Godwin Emefiele

Photographer: Chris J. Ratcliffe/Bloomberg

The Central Bank of Nigeria will likely hold its key rate at the July meeting of the monetary policy committee to allow the economy to recover, and might only start tightening in the fourth quarter of this year or early 2022. Although inflation remains at almost double the 9% top of the target band, Governor Godwin Emefiele said in May it’s driven by supply-side factors, including insecurity and poor infrastructure, and pressures will ease as domestic output grows.

The central bank has made it clear it wants to see a solid recovery before it will switch to fighting inflation, even as its under-pressure currency could benefit from higher rates.

What Bloomberg Economics Says:

“We think Nigeria’s inflation rate has reached its peak, and expect it to continue moderate in the coming months. Even so, we see it remaining stuck above target with policy makers hiking rates only later in the year once they are confident in the strength of the recovery. We have penciled in 4Q21 as the start of the hiking cycle, in line with the guidance given by the committee at the last meeting.”

--Boingotlo Gasealahwe

OTHER G-20 CENTRAL BANKS

Bank of Korea

- Current base rate: 0.5%

- Bloomberg Economics forecast for end of 2021: 0.75%

- Bloomberg Economics forecast for end of 2022: 1%

Lee Ju-yeol

Photographer: SeongJoon Cho/Bloomberg

The BOK looks set to raise its benchmark rate this year after Governor Lee Ju-yeol made clear that policy normalization was in the pipeline in 2021.

Investors and economists are looking at the fall for a move, likely to be Asia’s first post-pandemic shift. But there’s an outside chance it could even come this quarter. That means all commentary from central bank officials and their voting records will be carefully scrutinized over the coming months.

Another potential moment for further signaling of intentions or action comes in August when the central bank updates its growth and inflation projections.

While the economy has been growing faster than expected, the bank now sees asset bubbles and financial imbalances rising to a level that could imperil the recovery if left untamed. Inflation is also above its 2% target, though like many other central bankers, Lee has largely characterized the jump in prices as temporary.

What Bloomberg Economics Says:

“With South Korea’s recovery well underway, the BOK has made it crystal clear that policy normalization is nearing as it shifts its focus to mitigating financial risks. Even as it signals an impending hike, we don’t expect the central bank to rush its tightening process given its concerns about high household debt levels. Following a likely 25 bp hike in 4Q, we project one to two more increases in 2022.”

--Justin Jimenez

Reserve Bank of Australia

- Current cash rate target: 0.1%

- Bloomberg Economics forecast for end of 2021: 0.1%

- Bloomberg Economics forecast for end of 2022: 0.1%

Philip Lowe

Photographer: Brent Lewin/Bloomberg

The RBA is likely to open the quarter by extending its government bond-buying program while trying to draw a line on the duration of its yield curve control. Rates will stay put.

The strength of Australia’s recovery from the pandemic is giving the central bank little reason to let its control of three-year yields drift endlessly into the future. That’s why the vast majority of economists expect the RBA to opt against rolling over its yield-target bond to the November 2024 maturity from the current April 2024 -- a switch that would all but eliminate scope for raising rates before 2025.

The central bank’s quantitative easing will continue though. The bond buying has helped contain the currency, offering support for exporters and market stability. The debate is only over the form QE will take after September, with many economists expecting more flexibility on purchases.

What Bloomberg Economics Says:

“We expect rates to remain on hold through 2021, but the RBA is likely to be active in fine tuning policy settings. The RBA’s QE program is likely to be extended and adjusted, to curb currency appreciation and sustain the recovery. The surging housing market is likely to see the RBA working with other regulators to reinstate macroprudential policy restraints.”

--James McIntyre

Central Bank of Argentina

- Current rate floor: 38%

- Bloomberg Economics forecast for end of 2021: 38%

- Bloomberg Economics forecast for end of 2022: 35%

Miguel Pesce

Photographer: Maria Amasanti/Bloomberg

A policy shift at Argentina’s central bank is raising concerns about inflation ahead, as analysts anticipate larger monetary support to finance the nation’s treasury before midterm elections this year. Policy makers are now allowing commercial banks to exchange some of their central bank notes for treasury bonds, a move that risks further expanding the monetary base just as annual inflation hovers near 50%.

So far this year, the central bank has printed about one-fifth of the total 1.2 trillion pesos ($12.6 billion) it’s allowed to provide the treasury, according to the government’s budget. Analysts expect more fiscal spending ahead of a September primary vote and the general election in November. Inflation is forecast to end the year at 48%.

What Bloomberg Economics Says:

“The BCRA’s effort to tame inflation has been focused on capital controls to reduce peso depreciation, price controls, and other unorthodox measures. Our forecasts assume the BCRA will change its policy mix once it reaches a deal with the IMF -- likely in early 2022. If it succeeds in taming inflation, end-2022 rates could be lower than their current level.”

--Adriana Dupita

G-10 CURRENCIES AND EAST EUROPE ECONOMIES

Swiss National Bank

- Current policy rate: -0.75%

- Median economist forecast for end of 2021: -0.75%

- Median economist forecast for end of 2022: -0.75%

Thomas Jordan

Photographer: Stefan Wermuth/Bloomberg

The SNB’s monetary policy consists of negative rates and currency-market interventions, which central bank President Thomas Jordan deems most effective in light of the country’s small bond market.

Rosier prospects for a global economy helped the franc drop against the euro this year, a welcome development for the SNB which has spent years trying to tame the currency. So far, the pick up in inflation in other countries hasn’t been evident in Switzerland, where the headline rate is forecast to remain well within the SNB’s definition of price stability.

Sveriges Riksbank

- Current repo rate: 0%

- Bloomberg Economics forecast for end of 2021: 0%

- Bloomberg Economics forecast for end of 2022: 0%

Stefan Ingves

Photographer: Luke MacGregor/Bloomberg

Sweden’s central bank expects to keep its benchmark rate at zero all the way through the third quarter of 2024, even as the largest Nordic economy is in the midst of a robust recovery after having weathered the pandemic better than most rich nations. The rate forecast cements the Riksbank’s position as one of the most dovish among the G10 major currency holders.

The bank has held off on signalling a start to post-crisis hikes in borrowing costs as it’s still unsure of the virus outlook while inflation is seen falling short of target for years. The policy makers are also keen to avoid having to retrace tightening steps, something they were criticized for after the financial crisis by the likes of Nobel Prize winner Paul Krugman.

What Bloomberg Economics Says:

“Export-oriented Sweden was early to hike after the 2008 financial crisis, only to suffer a humiliating policy reversal because of a slide in inflation expectations. It won’t want to make the same mistake again. We see the Riksbank on hold while tapering asset purchases.”

--Johanna Jeansson

Norges Bank

- Current deposit rate: 0%

- Bloomberg Economics forecast for end of 2021: 0.5%

- Bloomberg Economics forecast for end of 2022: 1%

Oystein Olsen

Photographer: Kyrre Lien/Bloomberg

Norway’s central bank is preparing for a series of quarterly interest-rate increases, starting “most likely” in September. The June change toward a more hawkish outlook cements its outlier status among the rich peers in unwinding the crisis policies triggered by the pandemic.

The richest Nordic economy has been recovering faster than many developed nations, while Norges Bank Governor Oystein Olsen hasn’t needed to deploy any unconventional tools as the government is relying more than ever on the world’s largest sovereign wealth fund to boost stimulus. The recent strengthening of the krone has led to slower price gains, with underlying inflation dropping below the central bank’s 2% target in May for the first time since 2019.

What Bloomberg Economics Says:

“Oil-rich Norway faces a swift return to pre-pandemic levels and we expect Norges Bank to lift-off in September and hike again in December. High mortgage debt means consumers are likely to feel the pinch and we have pencilled in a slower pace of rate hikes in 2022.”

--Johanna Jeansson

Reserve Bank of New Zealand

- Current cash rate: 0.25%

- Bloomberg Economics forecast for end of 2021: 0.25%

- Bloomberg Economics forecast for end of 2022: 0.25%

Adrian Orr

Photographer: Mark Coote/Bloomberg

The RBNZ looks set to be in the vanguard of stimulus withdrawal after it became one of the first central banks to forecast rate increases next year. The bank’s reinstated projections for the official cash rate show it starting to rise in the second half of 2022.

The coming quarter is likely to see economists recalibrating their calls for that first move as they digest incoming data and the latest signaling from the central bank. Some analysts already point to a possible move in February and even the risk of a hike before the end of this year.

A surging recovery is helping fuel the rate hike expectations. The economy easily outperformed the RBNZ’s forecasts in the first quarter. Labor and goods shortages suggest inflation could accelerate toward the top of the RBNZ’s 1-3% target band.

What Bloomberg Economics Says:

“The RBNZ looks set to keep rates on hold in 2021, but policy tightening is likely on other fronts. Particularly macroprudential policy tools, with debt-to-income limits likely to be deployed over coming months to cool surging house prices. A tapering of RBNZ bond purchases is underway, though this is in response to smaller deficits and reduced bond supply rather than a shift in policy stance.”

--James McIntyre

National Bank of Poland

- Current cash rate: 0.1%

- Median economist forecast for end of 2021: 0.1%

- Median economist forecast for end of 2022: 0.5%

Adam Glapinski

Photographer: Piotr Malecki/Bloomberg

With consumer-price growth at the European Union’s second-highest level, expectations were rising in Poland that it would follow nations such as Hungary and the Czech Republic that -- alarmed by rising inflation -- raised rates. Governor Adam Glapinski though nixed such noise as he dismissed inflation as temporary and driven by factors beyond the control of the Monetary Policy Council. That allowed policy makers to not only keep the benchmark at 0.1% even as inflation hit a decade-high of 4.7%, but also to reiterate the pledge that borrowing costs won’t be changed possibly into 2022.

The Council, according to Glapinski, needs to see the nation’s economy sustained on the fast-growth track, and inflation still at elevated levels to start considering any monetary tightening.

Czech National Bank

- Current cash rate: 0.5%

- Median economist forecast for end of 2021: 0.75%

- Median economist forecast for end of 2022: 1.5%

Jiri Rusnok

Photographer: Martin Divisek/Bloomberg

The Czech central bank was the second one in the European Union’s eastern wing to lift borrowing costs in June, and signaled at least two more rate hikes by the end of the year. With the economy recovering faster than expected and many industries suffering from a shortage of workers , policy makers want to prevent higher commodity costs or supply chain bottlenecks from spilling into inflation expectations at home.

“We are concerned that part of these effects will stay in the economy permanently,” Governor Jiri Rusnok said after the June 23 rate hike. “We can’t expect them to peter out on their own. We are not that optimistic.”

— With assistance by Simon Kennedy, Niraj Shah, Ramsey Al-Rikabi, Anna Andrianova, Onur Ant, Theophilos Argitis, Dorota Bartyzel, Catherine Bosley, Matthew Brockett, Alister Bull, Toru Fujioka, Patrick Gillespie, Paul Gordon, Max De Haldevang, Michael Heath, Harumi Ichikura, Paul Jackson, Claire Jiao, Sam Kim, Cagan Koc, Peter Laca, Reed Landberg, Andrew Langley, Matthew Malinowski, Anirban Nag, Paul Richardson, Niclas Rolander, Nasreen Seria, Barbara Sladkowska, Alonso Soto, Ott Ummelas, Rene Vollgraaff, Alexander Weber, and Yinan Zhao

"easy" - Google News

July 04, 2021 at 06:01AM

https://ift.tt/3Arle0c

Beginning of the End of Easy Money: Central Bank Quarterly Guide - Bloomberg

"easy" - Google News

https://ift.tt/38z63U6

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

Bagikan Berita Ini

0 Response to "Beginning of the End of Easy Money: Central Bank Quarterly Guide - Bloomberg"

Post a Comment